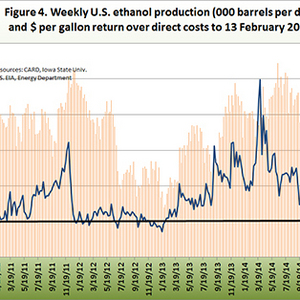

Economists examine recent trends in ethanol production, policy

AgMarketing Resource Center

March 3, 2015

BY Susanne Retka Schill

Advertisement

Advertisement

Related Stories

As part of the USGC’s strategy to support the initiation of the ethanol-gasoline blending program in Costa Rica, the group participated in a technical workshop in San Jose, Costa Rica, that focused on ethanol and vehicle compatibility.

Aemetis Inc. has announced it is implementing the Microsoft Dynamics enterprise resource planning (ERP) system worldwide for all Aemetis operations in the U.S. and India to support current operations and expansion projects.

Valero Energy Corp. on April 25 announced that its SAF project in Texas is progressing ahead of schedule and expected to be operational this year. The company also reported its ethanol and renewable diesel operations were profitable during Q1.

LanzaJet on April 22 announced an investment from Microsoft’s Climate Innovation Fund. This investment from Microsoft enables LanzaJet to continue building its capability and capacity to deploy its sustainable fuels process technology globally.

U.S. fuel ethanol production fell by 3% the week ending April 19, according to data released by the U.S. Energy Information Administration on April 24. Stocks of fuel ethanol were down 1% and exports fell by 23%.

Upcoming Events

@ Copyright 2024 - BBI International - All rights reserved.