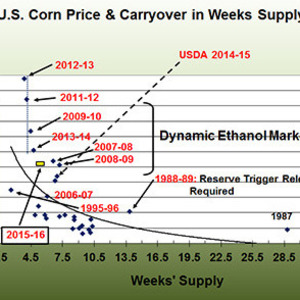

Ample corn supplies expected, modestly higher prices forecast

monthly Ag Marketing Resource Center

April 30, 2015

BY Susanne Retka Schill

Advertisement

Advertisement

Related Stories

The National Corn Growers Association is calling on entrepreneurs, researchers, and startups to reimagine the potential of field corn by entering the fifth round of the Consider Corn Challenge. Applications are due June 30.

The USDA recently released its Grain Crushings and Co-Products Production report for June, reporting that corn use for fuel ethanol in April was down when compared to the previous month, but up when compared to April of last year.

The 2025 International Fuel Ethanol Workshop & Expo, held in Omaha, Nebraska, concluded with record-breaking participation and industry engagement, reinforcing its role as the largest and most influential gathering in the global ethanol sector.

The USDA maintained its forecast for 2025-’26 corn use in ethanol production in its latest World Agricultural Supply and Demand Estimates report, released June12. The outlook for season-average corn prices was also unchanged.

SkyNRG on June 5 released its fifth Sustainable Aviation Fuel Market Outlook. The report, developed in collaboration with ICF, highlights the need to scale up technologies and feedstocks that are an alternative to HEFA fuels.

Upcoming Events

@ Copyright 2025 - BBI International - All rights reserved.